I catch a lot of flack for noticing things that might turn out badly but it happens that some things are better dealt with and prepared for before they totally screw things up. For the last year or more, it has been exceedingly hard to make any estimates about interest rates, prices or customer demand mostly because none of the really bad possible outcomes are even talked about much less discounted by the "markets"

Take for example the price of Gas & Diesel fuel. Business owners need to make plans and budgets which factor those costs moving forward over the next few quarters. Any unexpected shock to upside will ruin those estimates and cause huge dislocation and a wild scramble to adjust to the difference and secure supplies. The possibility of that happening due to the undeniable disruption in supplies from the Persian Gulf over the last four months is huge yet, the price of those commodities in the "markets" and also at the pump (POS) implies that the risk is non-existent or, at least not that immediate.

Industry experts in the Oil & Gas space many of whom have decades of experience and are paid huge sums by large companies and investment firms to "get it right" are rubbing their eyes in disbelief at the numbers. "Tank bottoms" is when we run out. Period. There are no ships in any ports with oil to replace the stocks when that time arrives which, according to these extremely experienced people will be in a few weeks. Not months or quarters....WEEKS!

Oil markets may be celebrating the U.S.-Iran peace deal too early, as reopening the Strait of Hormuz will not immediately restore tanker traffic, production, refining activity, or insurance coverage.

Global oil inventories have been heavily depleted during the Hormuz crisis, with analysts and industry executives warning that stocks are approaching critically low operational levels and will need to be replenished.

Back in May, Carlyle Group’s Jeff Currie warned that by July, parts of the world would face what he dubbed “minimum operational levels” of crude oil supply due to depletion resulting from storage withdrawals to avoid shortages amid the Hormuz crisis.

I don't want to talk about politics, this blog is meant to address important issues which are not partisan and whose purpose is to simply inform business owners what the facts are so they can plan accordingly. It sure doesn't help when the current President says things like this however:

Asked about the inflation spike, President Trump said, “I love the inflation,” while also saying he expected inflation to come down if the conflict with Iran ends.

Now, taken literally, that sounds absurd.

Nobody loves inflation! Certainly not the family paying more at the pump. Not the retiree watching grocery bills creep higher again. Not the worker whose raise disappears before it ever reaches the checking account.

But I think the remark matters for a different reason: It shows how difficult it’s become to explain inflation away.

Politicians don't see, hear or speak about inflation other that to dismiss it or explain how it's not a problem. That's true to some extent: It is not a problem for THEM.

But I digress...

Right now, business owners need to focus on things that help their businesses grow while, at the same time, stay aware of realities which could disrupt those plans. That doesn't require a "siege mentality" but simply acute awareness of their own industry including both opportunities and risks.

Asking questions like, "what do I do if fuel prices spike?" or "what is my policy on borrowing if interest rates aren't going back to 3%?" doesn't mean you're despairing, it means you're preparing! Comfort zones are nice but business owners rarely grow inside them but rather when they purposefully try new things or are either forced out but external factors imposed on them by, well, reality! My job is to give business owners actionable options they can act on with confidence. To do that I need to understand both current and past realities and hopefully extrapolate that information into a cogent plan of action that has a high possibility of success. That is, I could never be a politician or military planner.

For now, there is one reality which means whatever is happening at this moment in time. Fuel prices are stable to lower, inflation is out of hand even though the official numbers say otherwise and the cost of capital, which is my particular wheelhouse, are also uncomfortably stable and probably going higher. Lenders are skittish and unpredictable which makes things harder. Many of my clients are saying their banks with whom they have decades of relationships with are either reducing their lines of credit or eliminating them entirely. This is unsettling for many business owners but it's not always due to them or their business activity. Liquidity has become an acute problem with many banks and the Fed who is the last resort for banks is dragging their feet. The reasons for that are legion but the most critical one is that there a simply fewer buyers of US Treasuries at a time when the government needs to refinance a s**t-load of them. Banks have less money to lend unless the Fed gives it to them on the cheap because the Treasuries Banks are holding in their reserves are mostly under water - some are WAY underwater. That means booking a loss to access that capital and most banks simply couldn't survive that because it would make them insolvent. The Fed allows the banks to avoid reporting those losses by not requiring them to mark their Treasury holdings at market value. You read that correctly. Banks are allowed to carry losing Treasury positions at their original cost rather than market value making their financial position much stronger than it is in, yes, you guessed it....reality.

Nice work if you can get it.

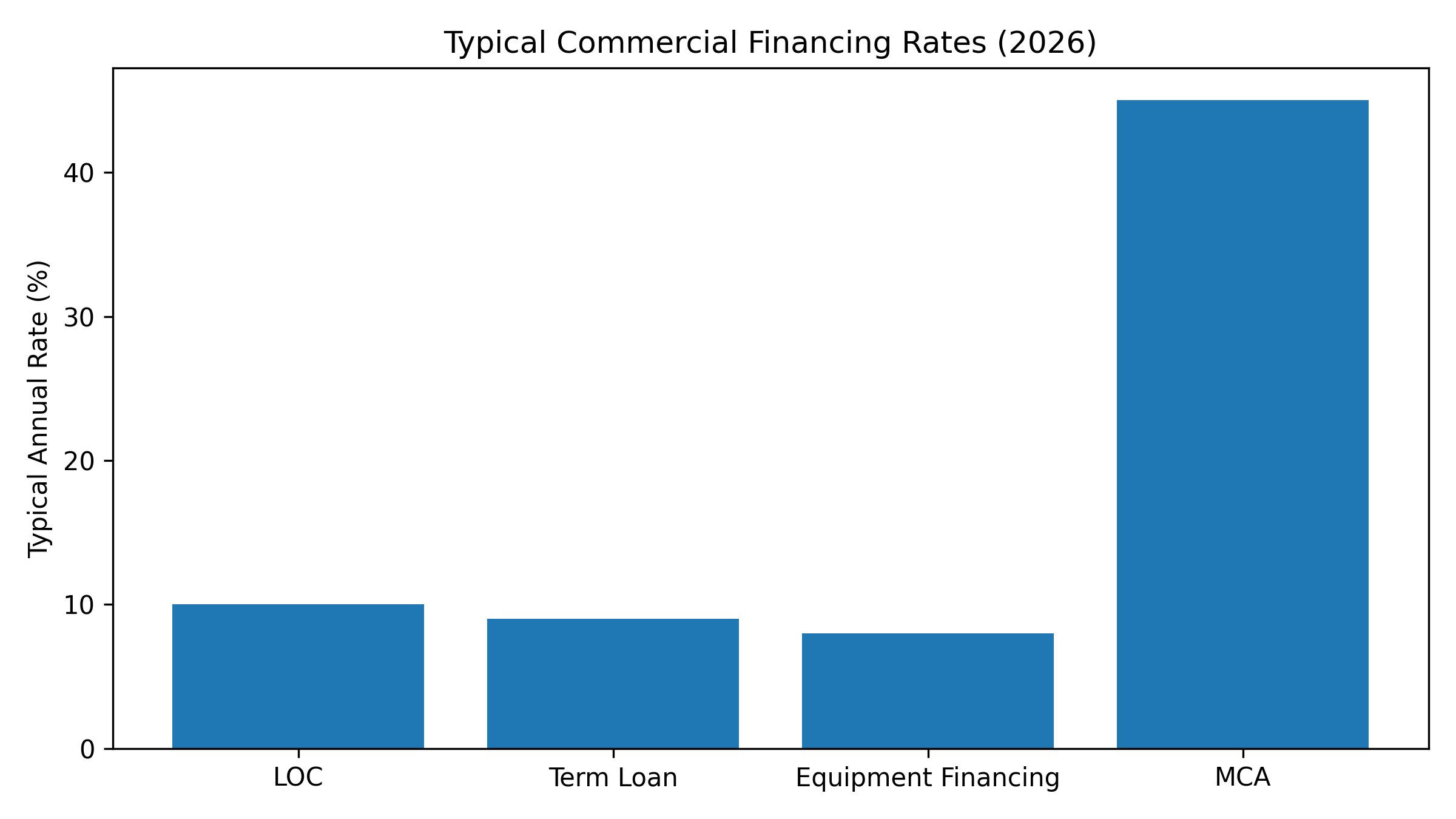

Here are this week's commercial rates:

MCA (Merchant Cash Advance) is reflected as APR however actual rates are factor rates which range between 1.2-1.5

Factor Rates on MCA loans haven't changed much in over 6 years mostly because they are already quite high but also because they represent the highest risk category of commercial loans. For many business owners paying MCA rates is unsustainable longer term however these loans serve a purpose in some situations and can actually be very beneficial to businesses that need some extra funding when they fall short. The main advantages MCA provide is 1. Speed - they can fund in 24 hours and 2. Unsecured - there's no collateral required which means they can be used to extend existing financing beyond what collateral valuations allow.

Call or message me for specific quotes, advice or just to bitch about life!

Please consider subscribing for this blog. I send one per week and I never share your info:

Here are some interesting articles I saw this week:

"The US has finally capitulated in its disastrously failed war against Iran, reportedly drafting a memorandum of understanding which is highly favorable to the Islamic Republic, and gains as concession nothing more than the promise that “Iran will not obtain nuclear weapons”—a position Iran had already long held."

"Since September 2022 the Fed has remitted nothing. Zero. For the first time since 1934.

The reason is simple: the Fed is losing money."